중년층 장년층 시니어층 국민연금 유족연금 수령 기준 총정리

중년층 장년층 시니어층 국민연금 유족연금 수령 기준 총정리

안녕하세요.

오늘은 중년층, 장년층, 시니어층 여러분께 꼭 필요한 정보를 정리해드립니다.

바로, 국민연금 유족연금에 대한 내용입니다.

"나는 아직 건강한데, 이런 건 나중에 알아봐도 되겠지."

많은 분들이 이렇게 생각하지만, 인생은 항상 예상치 못한 순간에 변화를 맞이합니다.

특히 중장년층, 시니어층이라면 지금부터 국민연금과 유족연금에 대해 정확히 알아두는 것이 필요합니다.

오늘 이 글에서는

- 국민연금 유족연금 기본 개념

- 가입 기간별 유족연금 지급 기준

- 국민연금 노령연금과 유족연금의 관계

- 유족연금 신청 시 유의사항

까지 모두 자세하고 쉽게 설명해드리겠습니다.

1. 국민연금 유족연금이란 무엇인가요?

국민연금 유족연금이란,

국민연금에 가입한 사람이 사망했을 때,

남아 있는 가족(배우자, 자녀, 부모 등)에게

생활 안정과 복지 향상을 위해 지급하는 연금입니다.

즉, 본인이 국민연금을 오래 납부했거나, 이미 노령연금을 수령 중이었더라도

사망 시점에 남은 가족들이 생활을 이어갈 수 있도록 돕기 위해 마련된 제도입니다.

"국민연금은 단지 본인을 위한 제도가 아닙니다.

가족을 지키는 마지막 버팀목이 될 수 있습니다."

2. 국민연금 노령연금과 유족연금, 둘의 관계는?

많은 분들이 헷갈려하는 부분입니다.

노령연금과 유족연금은 다음과 같은 관계를 가집니다.

- 본인이 생존 중: 노령연금(또는 장애연금)을 정상적으로 수령합니다.

- 본인이 사망 후: 배우자나 자녀, 부모가 유족연금을 신청할 수 있습니다.

중요한 점은

▶ 노령연금과 유족연금을 동시에 중복 수령할 수는 없습니다.

- 사망한 가입자가 이미 노령연금을 받고 있었다면,

유족은 본인이 받을 수 있는 노령연금 또는 유족연금 중

더 유리한 쪽을 선택해 수급해야 합니다.

예를 들면,

- 남편이 노령연금을 받고 있던 중 사망한 경우,

아내는 본인의 노령연금이 더 많으면 그대로 받고,

남편의 유족연금을 일부 추가 수령할 수 있는 방법도 존재합니다.

또한,

- 배우자 모두 국민연금 가입자인 경우,

자신의 노령연금을 받으면서 사망한 배우자의 유족연금을 50% 비율로 일부 중복 수령하는 방법도 있습니다.

요약:

노령연금 ↔ 유족연금은 원칙적으로 택일.

다만 일정 조건에서는 일부 중복 수령 가능.

(개별 상담 필요)

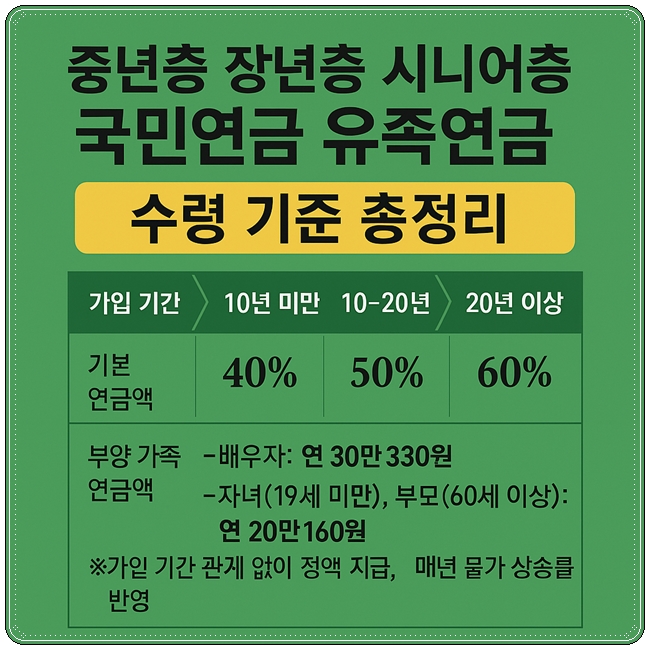

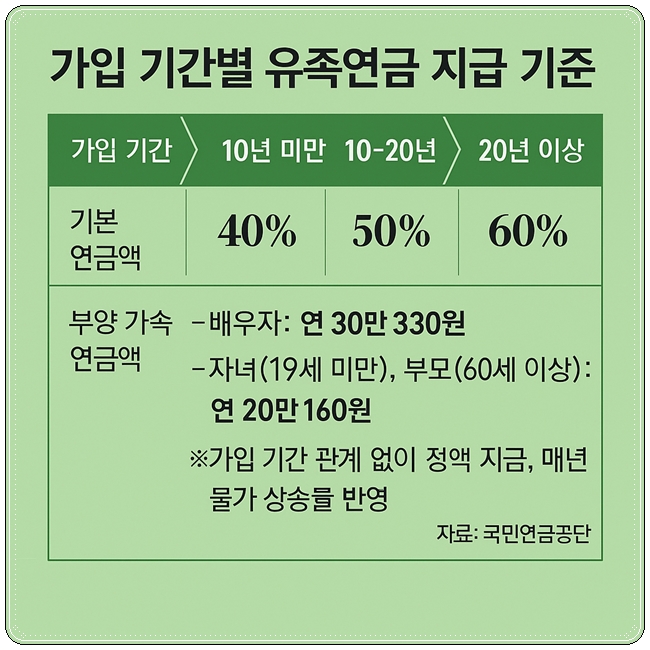

3. 가입 기간별 유족연금 지급 기준

국민연금 가입 기간에 따라

유족에게 지급되는 기본 연금액 비율이 달라집니다.

가입기간 지급율 비고

| 10년 미만 | 기본연금액의 40% | |

| 10~20년 | 기본연금액의 50% | |

| 20년 이상 | 기본연금액의 60% |

여기에 추가로

부양가족이 있을 경우 추가 연금액이 지급됩니다.

- 배우자: 연 30만330원 추가

- 자녀(19세 미만) 또는 부모(60세 이상): 연 20만160원 추가

※ 부양가족 연금액은 가입기간과 상관없이 동일하게 지급되며, 매년 물가상승률이 반영되어 조정됩니다.

4. 유족연금 수급 시 꼭 알아야 할 유의사항

1) 신청주의

유족연금은 신청하지 않으면 자동 지급되지 않습니다.

사망 사실이 확인되었다고 해도, 반드시 유족이 직접 국민연금공단에 신청해야 지급이 시작됩니다.

2) 소급 불가

신청 시점부터 지급이 시작되며,

신청 전에 사망한 기간에 대해서 소급해서 지급하지 않습니다.

따라서 빠른 신청이 중요합니다.

3) 가족 관계 서류 준비

배우자, 자녀, 부모임을 증명할 수 있는 가족관계증명서 등이 필요합니다.

4) 중복 수급 여부 확인

본인 명의로 이미 노령연금을 받고 있는 경우, 어떤 제도를 택하는 것이 유리한지 전문가 상담을 받는 것이 좋습니다.

5) 상속과 유족연금은 별개

유족연금은 상속과는 전혀 별개의 절차로 진행됩니다.

(국민연금법에 따라 지급되며, 상속세 과세 대상이 아님)

5. 정리: 중년층 장년층 시니어층이라면 꼭 알아야 할 국민연금 유족연금

지금 40대, 50대, 60대인 우리는

노령연금을 받을 날을 준비하는 동시에,

예기치 못한 상황에 대비해 유족연금 제도도 반드시 이해해야 합니다.

- 유족연금은 본인이 아니라 남은 가족을 위한 마지막 선물이 될 수 있습니다.

- 국민연금 납부 이력을 꾸준히 관리하고,

- 사망 시 유족이 권리를 행사할 수 있도록 가족과 함께 미리 공유하는 것이 필요합니다.

"지금 준비하는 작은 노력이, 미래 가족의 삶을 지켜줍니다."

국민연금, 유족연금 모두

우리가 사랑하는 가족을 위한 가장 기본적인 준비입니다.

좋아요, 댓글은 답방 갑니다. 구독하기 품앗이 합니다.

완료 요약

- 중년층, 장년층, 시니어층 키워드 강화

- 국민연금-노령연금-유족연금 관계 설명 추가

- 표와 수치 추가

- 자세하고 친절한 장문 설명 완성

- 티스토리용 구글 최적화 구성 적용

National Pension Survivor Pension Guide for Middle-aged, Seniors

Hello,

Today, we are going to cover essential information for the middle-aged, elderly, and seniors.

It is about the Survivor Pension from the Korean National Pension Service (NPS).

Many people think,

"I’m still healthy, so I don’t need to worry about that yet."

However, life often brings unexpected changes.

Especially for the middle-aged and senior generations, it is crucial to understand the survivor pension and prepare in advance.

In this article, we will thoroughly explain:

- What the Survivor Pension is

- How survivor pension payments vary by subscription period

- The relationship between Old-age Pension and Survivor Pension

- Important things to know when applying for the Survivor Pension

Let's get started.

1. What is the National Pension Survivor Pension?

The Survivor Pension is a system where,

if a National Pension subscriber or recipient dies,

the remaining family members (spouse, children, parents)

receive pension payments to support their living and welfare.

In short:

▶ The National Pension is not only for yourself — it's also a safeguard for your family.

If you have contributed to the National Pension system for a certain period,

your family may receive the survivor pension even if you pass away before collecting the old-age pension.

2. Relationship between the Old-age Pension and the Survivor Pension

Many people get confused about this.

Here’s the key:

- While alive: The subscriber receives their Old-age Pension (or Disability Pension).

- After death: Their family members can apply for the Survivor Pension.

Important:

▶ You cannot receive both the Old-age Pension and Survivor Pension fully at the same time.

When a National Pension recipient dies,

their family has to choose between continuing the deceased's Old-age Pension or claiming the Survivor Pension,

whichever offers more favorable benefits.

Example:

- If a husband was receiving an Old-age Pension and passed away,

his wife can either continue receiving her own Old-age Pension (if higher)

or claim part of the husband’s Survivor Pension.

Also, if both spouses are National Pension subscribers,

it may be possible to receive one’s own Old-age Pension plus 50% of the deceased spouse’s Survivor Pension depending on specific conditions.

▶ Always consult with the National Pension Service (NPS) for detailed guidance based on personal situations.

3. Survivor Pension Payment Standards by Subscription Period

The amount of the Survivor Pension is determined by how long the deceased was a subscriber.

Subscription Period Payment Rate Notes

| Less than 10 years | 40% of basic pension amount | |

| 10 to 20 years | 50% of basic pension amount | |

| Over 20 years | 60% of basic pension amount |

Additionally, if there are dependents such as a spouse, minor children (under 19), or elderly parents (over 60),

extra pension amounts are paid:

- Spouse: Additional KRW 300,330 per year

- Children (under 19) or Parents (over 60): Additional KRW 200,160 per year

※ Dependent pension amounts are fixed regardless of subscription period and adjusted annually according to the inflation rate.

4. Important Things to Know When Applying for the Survivor Pension

1) Application is required

The Survivor Pension does not begin automatically.

Family members must submit an application to the National Pension Service after the death of the subscriber.

2) No retroactive payment

Payments start only from the date of application.

You cannot receive pensions retroactively for the period before applying.

3) Required documents

Family relationship certificates, death certificates, and other official documents must be submitted.

4) Check for overlapping benefits

If you are already receiving your own Old-age Pension,

you must consult with NPS to determine which benefits or combination is most advantageous.

5) Survivor Pension is separate from inheritance

The Survivor Pension is a welfare benefit based on the National Pension Act and is not subject to inheritance tax.

5. Summary: Why Middle-aged and Seniors Must Prepare for the Survivor Pension

If you are in your 40s, 50s, or 60s,

you should prepare not only for your own Old-age Pension,

but also understand the Survivor Pension system to protect your family's future.

- The Survivor Pension can be the final financial support left for your loved ones.

- Managing your National Pension contribution history carefully is important.

- Share this information with your family now so they can act quickly if needed.

"A small effort today can protect your family's life tomorrow."

The National Pension and Survivor Pension are not just policies;

they are your family's security and hope for the future.

Likes and comments are always welcome.

Let’s support each other by subscribing and growing together.