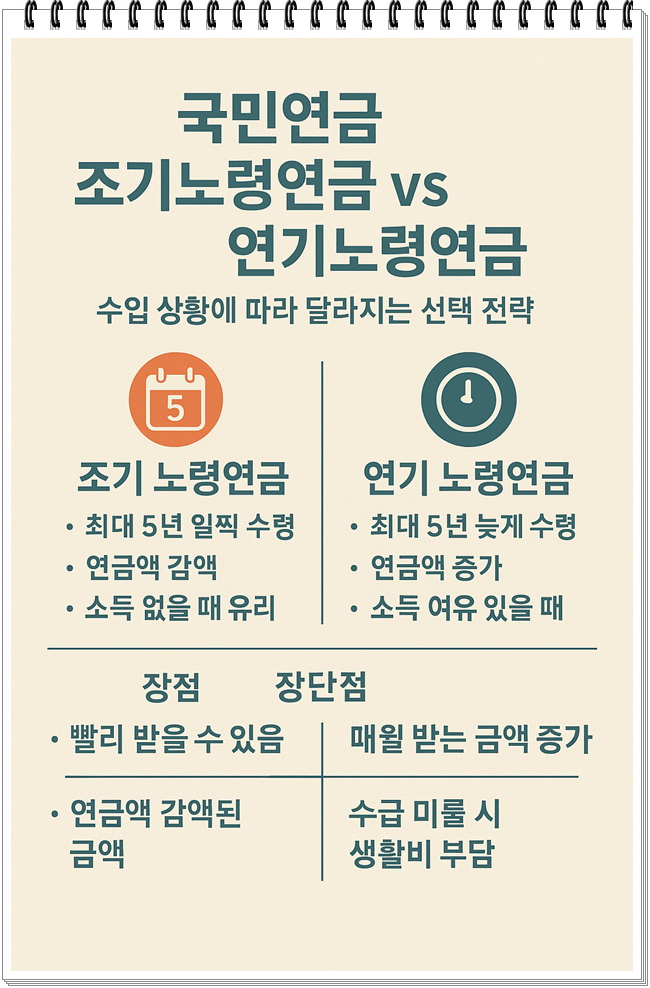

국민연금 조기노령연금 vs 연기노령연금, 수입 상황에 따라 달라지는 선택 전략

국민연금 조기노령연금 vs 연기노령연금, 수입 상황에 따라 달라지는 선택 전략

안녕하세요. 공간에서 세상으로 인사드립니다. 은퇴를 앞두고 가장 많이 고민하는 것 중 하나가 바로 국민연금을 언제 받는 것이 유리할까입니다. 오늘은 조기노령연금과 연기노령연금의 차이점과 장단점, 그리고 무엇보다 개인의 수입과 자금 상황에 따라 어떻게 선택해야 할지에 대해 정리해보겠습니다.

1. 조기노령연금과 연기노령연금, 무엇이 다른가요?

1) 조기노령연금이란?

국민연금 정해진 수급 나이보다 최대 5년 먼저(예: 만 60세부터) 받을 수 있습니다. 수령을 앞당긴 만큼 연금액이 1년당 5%씩 감액되어 최대 25%까지 줄어듭니다. 소득이 없을 때 조기 신청이 가능하며, 당장의 생활자금이 필요할 때 유리합니다.

2) 연기노령연금이란?

정해진 수급 나이보다 최대 5년 늦춰 받을 수 있는 제도입니다. 연기한 1년당 약 7.2%씩 증가하여 최대 36%까지 연금액이 올라갑니다. 수입이 있거나 자금 여유가 있을 때, 장기적으로 더 많은 금액을 받고자 할 때 선택됩니다.

2. 장단점 요약 비교

1) 조기노령연금의 장점

빨리 받을 수 있어 생활비 부족 시 유용합니다. 장수에 자신이 없거나 지병이 있는 경우 일찍 수령하는 것이 유리합니다.

2) 조기노령연금의 단점

평생 감액된 금액을 받습니다. 장수할 경우 총 수령액에서 손해가 될 수 있습니다.

3) 연기노령연금의 장점

수령 시기를 미루면 매월 받는 금액이 크게 증가합니다. 장수할수록 총 수령액이 커지고 노후 생활이 더 안정됩니다.

4) 연기노령연금의 단점

수급을 미루는 동안 다른 수입원이 없다면 생활비 부담이 클 수 있습니다. 수명이 짧을 경우 오히려 손해가 됩니다.

3. 수입 상황에 따른 선택 전략

국민연금 수령 시점은 개인의 소득 구조와 자산 여건에 따라 달라져야 합니다.

1) 소득이 전혀 없고 생활비가 빠듯한 경우

→ 조기노령연금이 유리합니다. 당장 생계를 위해 연금을 활용해야 하는 경우, 감액을 감수하고라도 수급을 앞당기는 것이 현실적입니다.

2) 소득이 있거나 퇴직금, 금융 자산 등 여유 자금이 있는 경우

→ 연기노령연금이 더 유리합니다. 5년을 연기하면 최대 36% 증가된 금액을 받게 되며, 장기적인 노후자금 설계에 있어 효율적인 선택이 됩니다.

3) 파트타임이나 일용직 등 소득이 작지만 꾸준히 있는 경우

→ 혼합 전략도 고려할 수 있습니다. 일부만 먼저 받고, 나머지는 연기하는 방식도 가능합니다.

4. 실제 수령액 비교 (가정 예시)

기준 연금액: 월 100만 원

정시 수급: 만 63세

조기 수급: 만 60세 (25% 감액 → 월 75만 원)

연기 수급: 만 68세 (36% 증가 → 월 136만 원)

기대수명: 85세 기준

→ 총 수령액 기준으로 보면

조기 수급은 약 2억 2천만 원,

정시 수급은 약 2억 6천만 원,

연기 수급은 약 2억 7천 8백만 원으로

장수할수록 연기 수령이 유리합니다.

하지만 수입이 없는 상황에서는 조기 수령이 실리적일 수 있습니다.

5. 정리하며 – 내 상황에 맞춘 ‘맞춤형 연금 전략’이 중요합니다

국민연금 수령 전략은 ‘일찍 받느냐, 나중에 받느냐’의 문제가 아닙니다. 지금의 소득 상태, 자산 보유 현황, 건강 상태, 기대 수명, 그리고 은퇴 후 계획을 종합적으로 고려해 결정해야 합니다. 당장의 생활비가 급하다면 조기 수령이, 노후에 안정적인 소득을 늘리고 싶다면 연기 수령이 당신의 인생 설계에 도움이 될 것입니다.

좋아요, 댓글은 답방 갑니다. 구독하기 품앗이 합니다.

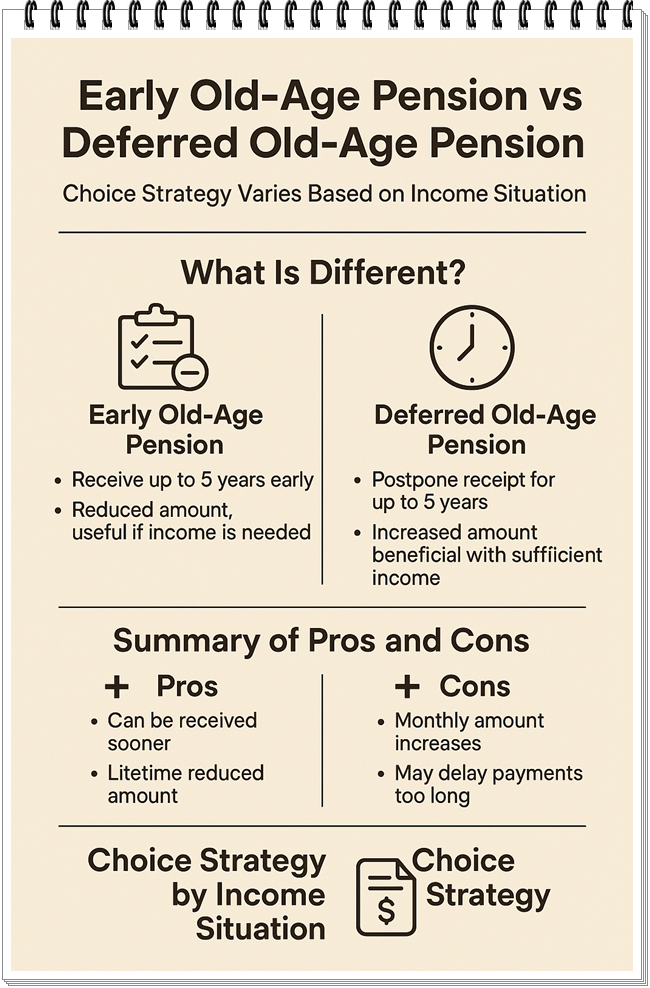

Early Pension vs. Deferred Pension in Korea: Choosing the Best Strategy Based on Your Income Situation

Hello. Greetings from "Space to the World."

One of the biggest concerns when approaching retirement is when to start receiving the National Pension. Today, we will summarize the differences, pros and cons between early pension and deferred pension, and more importantly, how to choose according to your income and financial situation.

1. What is the Difference Between Early Pension and Deferred Pension?

1) Early Pension

You can start receiving your pension up to 5 years earlier than the official age (e.g., from age 60). Your pension amount will be reduced by 5% for each year you receive early, up to a maximum reduction of 25%. It is advantageous when you have no income and need immediate living expenses.

2) Deferred Pension

You can choose to delay your pension up to 5 years past the official age. Your pension amount increases by about 7.2% for each year of deferral, up to a maximum of 36%. It is suitable if you have other income or financial resources and want to maximize your long-term pension amount.

2. Summary of Pros and Cons

1) Advantages of Early Pension

You can receive payments sooner, which is helpful when living expenses are tight. If you have health concerns or a lower life expectancy, early receipt can be beneficial.

2) Disadvantages of Early Pension

You will receive a permanently reduced pension amount. If you live longer, you may end up receiving less in total.

3) Advantages of Deferred Pension

The longer you defer, the larger your monthly pension becomes. If you live longer, your total pension received increases significantly, securing a more stable retirement.

4) Disadvantages of Deferred Pension

If you have no other income during the deferral period, your living expenses may be strained. If life expectancy is shorter, it may lead to financial loss.

3. Choosing Based on Income Situation

The timing of receiving the National Pension should be adjusted based on individual income and asset conditions.

1) If You Have No Income and Tight Living Expenses

→ Early pension is better. Accept the reduced amount to secure immediate cash flow.

2) If You Have Income or Sufficient Financial Assets

→ Deferred pension is better. Delaying up to 5 years will increase your pension amount by up to 36%, making it a wise long-term financial strategy.

3) If You Have Small but Steady Income (Part-time, Day Labor, etc.)

→ A mixed strategy can be considered. You may start receiving a portion early and defer the rest.

4. Actual Pension Amount Comparison (Example)

Base pension amount: 1 million KRW per month Normal starting age: 63 Early starting age: 60 (25% reduction → 750,000 KRW) Deferred starting age: 68 (36% increase → 1,360,000 KRW) Life expectancy: 85 years

→ Total pension received: Early pension: about 220 million KRW Normal pension: about 260 million KRW Deferred pension: about 278 million KRW

Thus, the longer you live, the more advantageous the deferred pension becomes. However, if you have no income, early pension may be a more realistic choice.

5. Conclusion - Customized Pension Strategy is Essential

The decision of when to start receiving the National Pension is not simply about "earlier or later." It must comprehensively consider your current income, asset holdings, health condition, expected lifespan, and retirement plans. If immediate living expenses are urgent, early pension is helpful. If you aim for a stable and increased income during retirement, deferred pension will be a valuable strategy for your life planning.

Likes and comments are welcome. Subscriptions are mutual support.

National Pension, Early Pension, Deferred Pension, Retirement Planning, Pension Strategy, Old Age Pension, Income Strategy, Financial Planning, Pension Comparison, Senior Income